The Supreme Court of Ghana, Accra, 2016.

The courtroom smelled of old paper and conditioning air that had been recycled too many times. Three justices sat elevated behind the bench, their faces arranged in the particular blankness that senior jurists develop after years of hearing arguments that arrive with great ceremony and depart with very little resolution.

On the table before the lead counsel for one of the respondents sat a folder. It had been photocopied so many times that its original ink had softened into grey approximations of itself. The documents inside dated back eight years. Some of the lawyers in the room had still been in secondary school when the events described inside that folder first occurred.

The lead counsel opened it slowly.

The folder contained the reconstruction of a single Friday afternoon in May 2008. A single transaction. Approximately 14.3 million shares in CAL Bank. A buyer, a seller, a broker, a settlement bank, a registrar, and a regulator whose intervention would eventually become one of the most disputed timing questions in Ghanaian commercial legal history.

The justice in the centre adjusted his glasses and looked down at the document before him.

He read the critical paragraph twice.

Then he looked up at the room.

What he was about to ask would take years to answer. And the answer, when it finally arrived, would quietly alter how Ghana’s financial institutions understood timing, sequence, and legal reality itself.

Because this was no longer merely a dispute about shares.

Now it was a dispute about when reality becomes irreversible inside a financial system.

His mother used to say he was the quietest child she had ever raised.

Not quiet in the way of frightened children. Quiet in the way of someone who had already discovered that observation yields more power than performance.

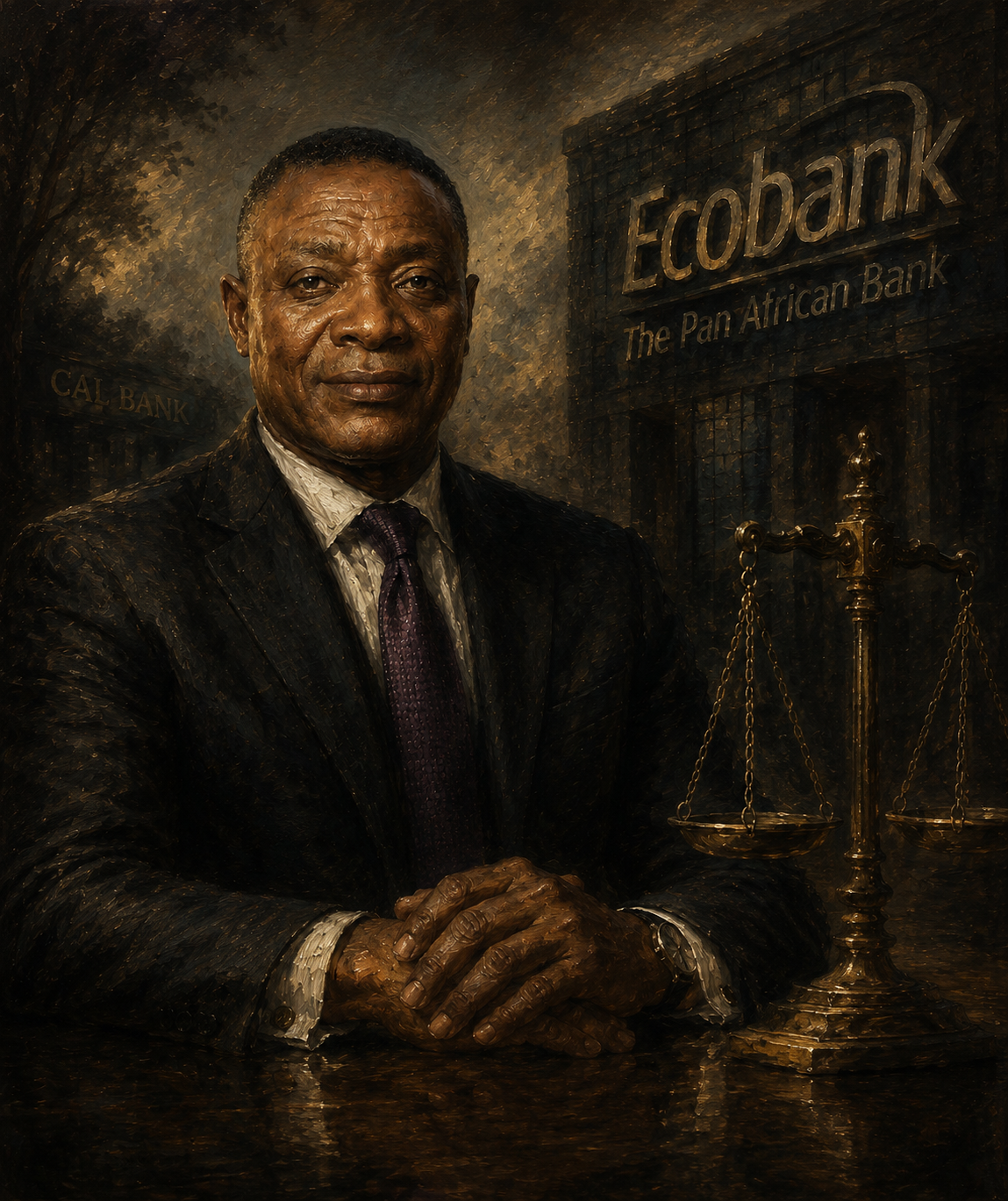

Daniel Kwame Ofori grew up in Kumasi during the 1970s and early 1980s, the son of a cloth trader whose stall sat near one of the older corridors of the Kumasi Central Market. Close enough to the main commercial flow to observe everything. Far enough from the center to avoid the dangerous attention that follows visible success in volatile trading environments.

It was, in retrospect, the perfect education.

The Kumasi market was not merely commerce.

It was information architecture.

The men who truly controlled the market were not always the loudest men. They were not always the richest-looking men either. But they understood pressure. They understood movement before movement became visible. They sensed shortages before shortages arrived. They knew which traders were expanding too aggressively, which suppliers were overexposed, which men were one bad month away from collapse.

Daniel watched them constantly.

After school, he would sit behind his father’s stall pretending to complete mathematics exercises while quietly studying human behavior instead.

He watched how prices changed depending on who approached a stall.

He watched how debt altered posture before it altered speech.

He watched how certain men entered negotiations already defeated.

And he watched one trader more carefully than the others.

A man named Acheampong.

Acheampong controlled one of the largest dry goods operations in that corridor. Yet he was never seen hurrying. He arrived at the same time every morning. He spoke softly. He rarely inspected inventory publicly. He left before the evening rush.

Yet somehow every meaningful transaction in that part of the market eventually moved through him.

“Why does everybody go to Acheampong?” Daniel once asked his father.

His father looked up slowly from his ledger book.

“Because he knows where the pressure lives.”

Daniel wrote the sentence quietly into the margin of his exercise book.

He was eleven years old.

There was one afternoon he would remember years later even after Kumasi itself had become emotionally distant to him.

A trader named Adu had overextended himself into imported fabric inventory he could not move quickly enough. By that stage, the debt was already visible before anyone confirmed it publicly.

His conversations had shortened.

His laughter had disappeared.

He kept checking the entrance of the corridor.

Then two men arrived.

They did not shout.

They did not threaten him publicly.

They simply stood at the stall in a very specific formation and spoke to him quietly.

Twenty minutes later, Adu began removing inventory from his shelves.

By evening, the stall looked hollowed out.

Adu himself looked smaller somehow, as though part of him had already been repossessed before the merchandise fully was.

Daniel watched everything from behind his father’s stall without touching his homework.

He did not watch with excitement.

He watched with recognition.

Because what he saw was not cruelty.

It was sequence.

A man had crossed invisible financial thresholds without fully understanding how irreversible they had become.

That realization settled deeply inside him.

Years later, it would return with terrifying familiarity.

Daniel Ofori was not remembered as a spectacular student.

He was remembered as careful.

Deliberate.

Suspicious of fast conclusions.

What he possessed early was not theatrical brilliance but systems intelligence. He understood instinctively that markets had hidden grammars beneath visible activity. That institutions behaved differently under pressure. That timing mattered more than appearances.

He left Kumasi for Accra carrying modest savings, disciplined habits, and years of quietly observing how commercial systems truly functioned beneath their surface performance.

He arrived in a capital city that was changing rapidly.

And he arrived prepared.

What he could not have known then was that one Friday afternoon decades later would force Ghana’s entire financial system to confront the exact lesson Kumasi had already taught him as a boy:

The moment something becomes irreversible is rarely the moment people realize it has happened.

Accra in the late 1980s was remaking itself unevenly.

Structural adjustment programs had begun reshaping the economy. Imported goods carried psychological significance beyond utility. Western clothing had become associated with movement, legitimacy, and social arrival.

Daniel Ofori noticed this almost immediately.

He understood something many retailers missed entirely:

people were not merely buying clothing.

They were buying future identity.

He began modestly. A small retail operation. Careful inventory choices. Relentless attention to customer behavior.

The store worked.

Not dramatically at first.

Carefully.

Which is how durable systems usually begin.

White Chapel Limited eventually expanded into one of Ghana’s defining retail names of its era. Long before Accra’s modern mall culture emerged fully, White Chapel had already learned how aspiration could be displayed, packaged, and monetized.

The company grew methodically.

Retail funded property acquisition.

Property generated rental income.

Rental income funded expansion.

Expansion reinforced brand visibility.

The system fed itself.

Daniel Ofori rarely behaved like a flamboyant businessman during those years. Associates described him instead as intensely observant. The loudest people in commercial systems are often performing confidence for spectators. The truly dangerous operators are usually the quieter men studying the room while others speak.

“He did not seem interested in looking successful,” one associate later recalled.

“He seemed interested in understanding how success actually worked.”

That distinction would eventually matter enormously.

By the early 2000s, Daniel Ofori had shifted deeper into Ghana’s capital markets.

The Ghana Stock Exchange was becoming more than a financial platform. Ownership inside listed institutions carried a form of national economic legitimacy. Banking stocks especially represented influence, access, and institutional permanence.

Daniel Ofori accumulated positions carefully.

Not recklessly.

Not emotionally.

Carefully.

He studied management behavior. Loan books. Institutional discipline. Market psychology.

Eventually he accumulated approximately 14.3 million shares in CAL Bank.

It was a significant position.

The kind institutions notice quietly.

The kind that alters the temperature of conversations in banking rooms once your name enters them.

By then, Daniel Ofori was no longer simply a businessman.

He had become part of Ghana’s financial architecture itself.

And architecture, once sufficiently connected to other systems, becomes vulnerable to failures occurring far away from where the original structure was built.

William Oppong-Bio moved quickly.

In the spring of 2008, he wanted a major position in CAL Bank shares. The market looked optimistic. Banking stocks were attractive. Momentum inside Ghana’s financial sector still felt strong.

Discussions began.

Databank Brokerage would facilitate the transaction. Ecobank would act as settlement bank.

The structure appeared straightforward.

Approximately 14.3 million CAL Bank shares would transfer from Daniel Ofori’s holdings to William Oppong-Bio.

The settlement date was scheduled for Friday, 30 May 2008.

Nobody involved appears to have believed the transaction would become historic.

That is important.

Because the most dangerous financial events rarely announce themselves in advance.

They arrive disguised as ordinary procedure.

Inside Ecobank, the settlement process moved forward normally.

A relationship manager reviewed settlement instructions. Internal approvals were processed. Documentation advanced through operational channels with the familiar rhythm of institutional routine.

At the registrar’s office, transfer preparations were also underway.

Everything still appeared synchronized.

That synchronization would later become the most important illusion in the entire case.

Because somewhere else inside Ghana’s regulatory architecture, concern had already begun forming.

Quietly.

The Bank of Ghana was reportedly becoming uncomfortable with aspects surrounding the transaction.

The precise timing of when concern evolved into intervention would later become one of the most litigated sequence questions in Ghanaian commercial history.

At the time, however, nobody fully understood what was approaching.

Everyone still believed they were preparing a transaction.

They were actually preparing a future courtroom reconstruction.

Accra carried a thick heat that Friday.

Office workers settled beneath weak air conditioners. Drivers waited outside commercial buildings with engines idling. Phones rang continuously across banking halls and brokerage offices while documents moved through the city in sealed envelopes and courier bags.

Inside Ecobank, settlement preparations were underway.

Inside the registrar’s office, the transfer documents arrived before midday.

Procedurally, the day still looked ordinary.

That was the deception.

Because sophisticated systems rarely collapse immediately after the first fracture appears. They continue functioning. They continue processing. They continue behaving as though synchronization still exists even after different parts of the machinery have quietly begun drifting apart.

At approximately 2:51 PM, the registrar began processing the CAL Bank transfer documentation.

Verification followed.

Approval followed.

Inside Ecobank, settlement instruments were being prepared simultaneously.

The machinery was moving.

At approximately 3:47 PM, the registrar’s stamp came down.

The shares had officially moved on the register.

At that exact moment, nobody inside the system fully understood that one of the most consequential legal timing questions in Ghanaian banking history may already have been decided.

Across the city, another meeting was ending.

Inside that meeting sat growing regulatory concern surrounding the transaction.

A decision had reportedly been reached.

Communication needed to move quickly.

Calls were made.

Instructions were dispatched.

But by the time the regulatory communication finally arrived at Ecobank, the transactional machinery may already have crossed legally irreversible thresholds.

The difference was approximately sixteen minutes.

Sixteen minutes.

In ordinary life, sixteen minutes is nothing.

Inside financial systems, sixteen minutes can alter millions of cedis, redefine ownership, and trigger litigation lasting nearly two decades.

By Monday morning, Ghana’s financial system would no longer fully agree on what reality legally was.

And once sophisticated institutions stop agreeing on reality, the danger begins quietly.

Not with collapse.

With contradiction.

The money freezes.

The market reacts.

And inside Ecobank, one ordinary banking question would later become one of the most dangerous moments in Ghanaian commercial litigation.

Start reading Part Two soon on Africa Reporters Network.

Note:

If this story stayed with you after reading, help us keep building work like this.

MoMo: 0248484405- Eykrom Company Limited

Bank: First national Bank

Account Name: Eykrom Company Limited

Acct Number: 1021005307101

Branch: Accra Main.

Branch Code 330103

Swift Code FIRNGHAC

Africa’s trusted news source.

.png)

Stay informed with the latest African media trends, job opportunities, and development news. Connecting Africa with global media and development partners.

)%20(1).jpg)

.avif)

.png)