Ghana’s telecom industry is a liberalized, infrastructure-heavy market that has moved from analogue mobile telephony in the early 1990s to a three-MNO structure today, with mobile voice deeply penetrated, mobile data still growing quickly, fixed voice in structural decline, fiber broadband still small in national penetration terms, and LEO satellite broadband now emerging as a real but still niche substitute in selected segments. The latest public subscriber statistics available are the National Communications Authority’s Q4 2025 bulletin, published in June 2026; the latest full-year public operator financials in this research set are MTN Ghana’s FY 2025 results; and the latest Starlink retail pricing referenced here is from Starlink’s Ghana pages visible in June 2026.

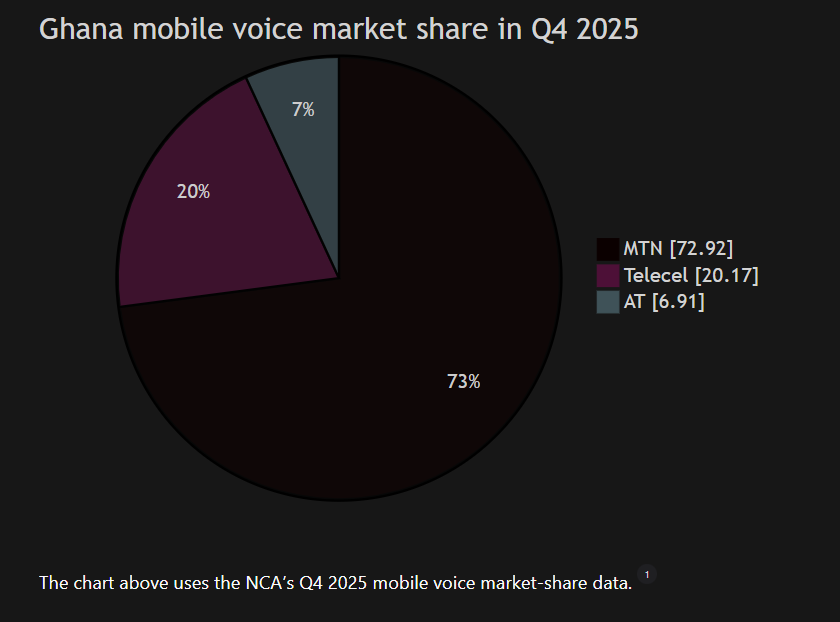

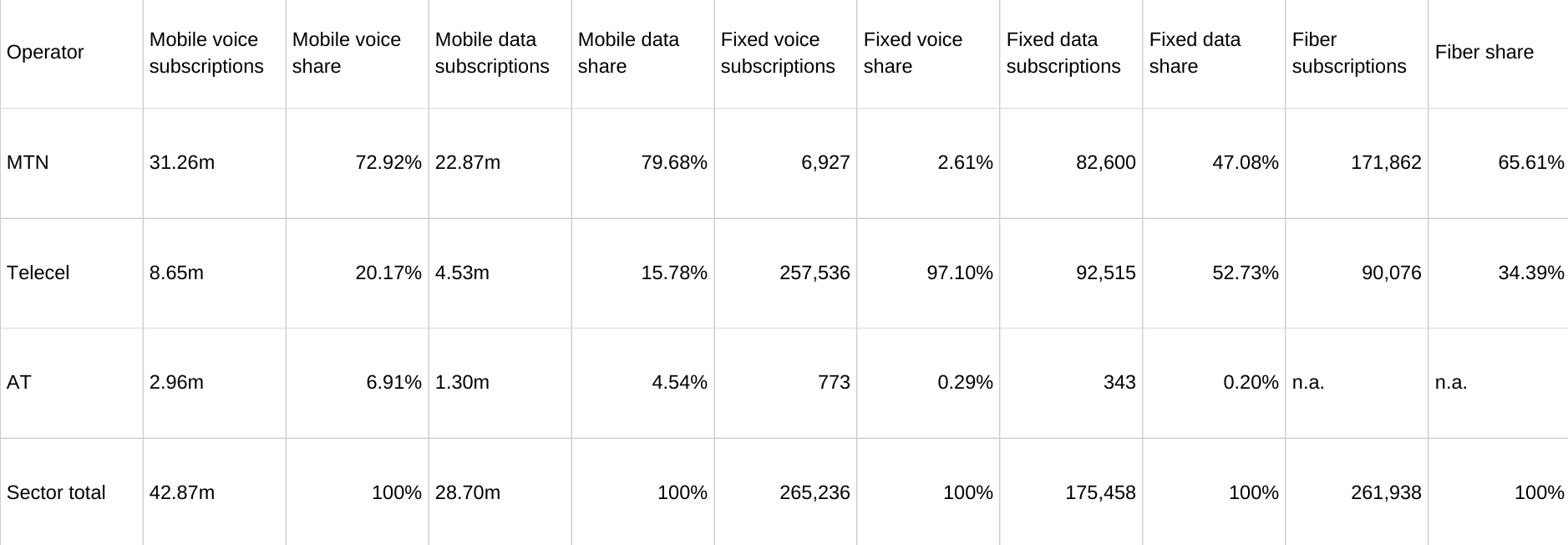

At the end of Q4 2025, Ghana had 42.87 million mobile voice subscriptions, 28.70 million mobile data subscriptions, 265,236 fixed voice subscriptions, 175,458 fixed data subscriptions, 261,938 fiber broadband subscriptions, and 22,706 Starlink satellite broadband subscriptions. MTN remained overwhelmingly dominant with 72.92% of mobile voice subscriptions and 79.68% of mobile data subscriptions; Telecel was the clear number two with 20.17% of voice and 15.78% of data; and AT had 6.91% of voice and 4.54% of data. In fixed voice, Telecel retained 97.10% share, while in fiber broadband MTN led with 65.61% against Telecel’s 34.39%.

The commercial center of gravity has decisively shifted from voice to data. MTN Ghana’s FY 2025 numbers are the clearest public proof point: service revenue grew 36.2% to GHS 24.36 billion, but data revenue rose 48.8% to GHS 13.36 billion while voice revenue increased only 7.8% to GHS 3.81 billion. At the same time, NCA data show sector mobile-data traffic rose to 1,101,301 TB in Q4 2025, while fixed voice subscriptions fell to just 265,236. In plain language, voice remains a cash-flow product, but data is the investment case.

The market is also extremely concentrated. A simple Herfindahl-Hirschman Index calculated from public Q4 2025 shares is about 5,772 for mobile voice and 6,619 for mobile data, reflecting a market structure in which MTN’s scale advantage is not marginal but structural. That concentration explains why regulation has focused on Significant Market Power remedies, national roaming, and the treatment of new wholesale and satellite entrants.

Fiber remains strategically important but nationally under-penetrated. Using the NCA’s Q4 2025 fiber-broadband total of 261,938 and the population base of 33,750,036 used in the same bulletin, implied national fiber-broadband penetration is roughly 0.78% of population. In the latest Communications Industry Report, Ghana reported 8,525.9 Gbps of submarine capacity available in 2024 and 51,552 Gbps of domestic terrestrial fiber capacity available, with MTN dominating inland fiber use. Yet public evidence still suggests that commercial FTTH/FTTB is concentrated in urban and peri-urban corridors rather than nationally dispersed.

Starlink is no longer hypothetical in Ghana. The NCA approved Starlink in April 2024 and announced official operations by the end of August 2024. By Q4 2025, Starlink had 22,706 Ghana subscriptions, with nearly 40% concentrated in Greater Accra and another 18.7% in Ashanti. Official Ghana-facing Starlink pricing visible in June 2026 showed Residential service starting from GHS 500 per month and a Mini Kit at GHS 2,200, far below the earlier standard kit price of GHS 5,390 published in the NCA’s 2024 Starlink FAQ. This price compression makes Starlink a credible threat in high-usage residential, SME backup, and underserved-rural segments, but not yet a mass substitute for nationwide prepaid mobile data.

For operators and investors, the strongest opportunities are in data capacity, enterprise and wholesale connectivity, fiber densification in commercially viable zones, tower power efficiency, and hybrid terrestrial-satellite resilience products. The biggest risks are continuing market concentration, uncertainty around AT’s restructuring, spectrum and 5G policy shifts, fiber-cut and power-cost exposure, and selective substitution by LEO services where terrestrial networks are weak or overpriced for heavy users.

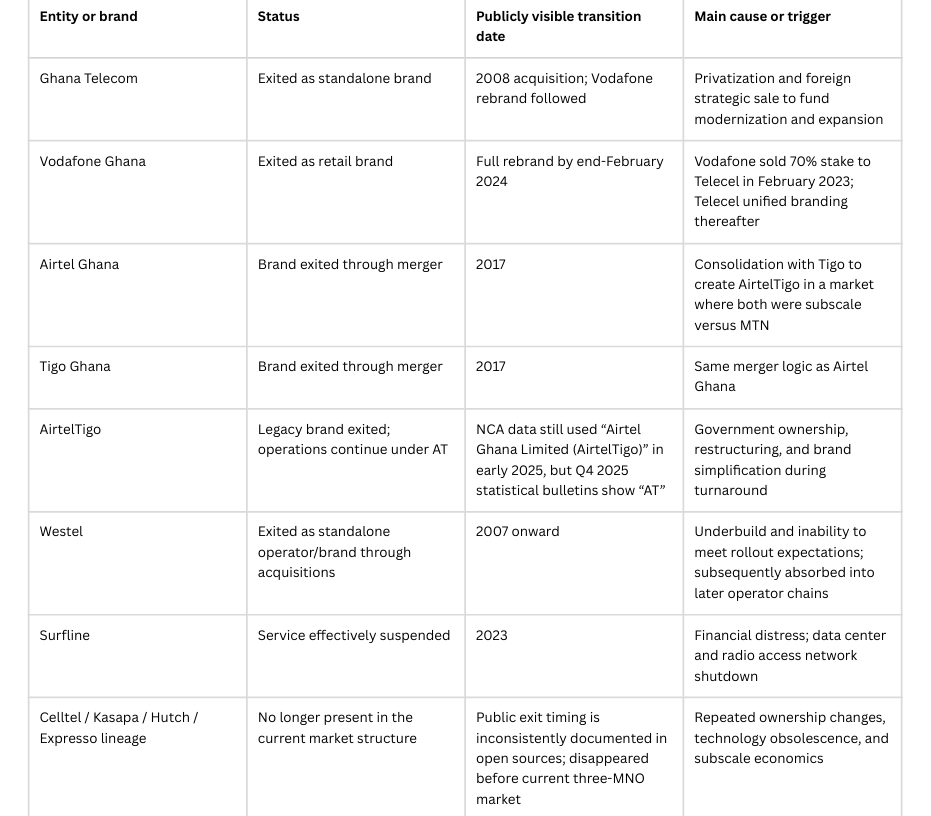

Ghana’s telecom market moved in distinct phases: monopoly-era fixed telephony; early analogue mobile competition in the 1990s; formal liberalization and regulation in the mid-1990s; privatization and foreign strategic investment in the 2000s; 3G/4G-led mass data adoption in the 2010s; and a new 2024-2026 phase centered on wholesale 5G design, SMP remedies, and satellite entry. The World Bank’s Ghana reform study identifies December 1996 as the point at which Ghana partially privatized Ghana Telecom and licensed a competing operator, while the NCA notes that it was established in 1996 to regulate communications activities. The NCA also records Ghana’s first 1G mobile launch by Mobitel in April 1992 and the launch of GSM in 1996 by Scancom under the Spacefon brand.

The most important structural break in sector history was the transformation of Ghana Telecom from a legacy incumbent into a succession of internationalized operators. Vodafone bought 70% of Ghana Telecom in 2008 for US$900 million, and Vodafone later sold that 70% stake to Telecel Group in February 2023; Telecel then completed the countrywide rebrand from Vodafone to Telecel by the end of February 2024. That lineage matters because today’s leading fixed-line base and much of the legacy fixed infrastructure still sit in that corporate chain.

A second defining theme has been the repeated inability of subscale challengers to remain sustainable as standalone operators. Ghana’s current number-three mobile operator is effectively the product of repeated restructurings in the Airtel/Tigo lineage, and the Ministry’s September 2025 briefing makes clear that AT’s situation had become severe enough that the regulator ordered national roaming onto Telecel’s network after a tower-power disconnection dispute tied to debt of more than US$150 million. Ghana’s telecom history is therefore not just one of liberalization, but of repeated consolidation, recapitalization, and emergency restructuring in the face of MTN’s persistent scale advantage.

Source note: Ghana Telecom/Vodafone/Telecel transitions are supported by Vodafone, Reuters, and Telecel sources; AT and AirtelTigo evidence comes from NCA market data and Ministry briefings; Westel’s historical underbuild and later acquisition are reflected in state and operator history sources; Surfline’s shutdown is documented by DatacenterDynamics and Graphic. The Kasapa/Expresso row is included because it is a widely recognized historical lineage in Ghana telecom history, but public exit dating is materially weaker than for the other rows.

The latest official public market structure is straightforward at the retail-network level: Ghana has three mobile network operators in NCA statistical reporting — MTN, Telecel, and AT — plus a now-material satellite broadband entrant, Starlink. The fixed voice and fixed data segments are also reported only for Telecel, MTN, and AT in the latest NCA bulletin. Public market-share data for the fragmented ISP and enterprise-connectivity layer remain far less transparent than the MNO layer.

The concentration is stark. Using the public Q4 2025 market shares above, implied HHI is roughly 5,772 in mobile voice and 6,619 in mobile data. Even without invoking any external competition threshold, those scores describe a market where concentration is structurally high, not merely above average. That is consistent with the NCA’s 2020 decision to designate MTN as a Significant Market Power operator and with the subsequent focus on roaming and other ex ante remedies.

Starlink should now be treated as a meaningful fourth retail access platform in broadband, though not a fourth MNO. At the end of Q4 2025, Starlink had 22,706 subscriptions in Ghana. Relative to the combined fiber-plus-Starlink access base of 284,644 subscriptions, Starlink already represented about 8.0% of that broader residential/business broadband pool. That is still small versus mobile and smaller than fiber, but it is no longer immaterial.

Outside the NCA’s core mobile/fixed tables, the surviving connectivity ecosystem includes wholesale and enterprise-fiber operators such as MainOne, C-Squared Ghana, Spectrum Fibre, and Comsys, plus retail ISPs and fixed-wireless providers such as Busy, Telesol, and Blu. NGIC is now the state-backed wholesale 4G/5G platform under development. Public subscriber shares, retail revenues, and customer counts for these non-MNO players are generally not disclosed in the primary sources used here; this is a major transparency gap in Ghana’s market data.

The lack of public subscriber and revenue reporting for non-MNO ISPs matters analytically. It means that regulator-published market concentration is easiest to observe in mobile and operator-owned fixed access, but much harder to quantify in enterprise internet, leased-line, metro-fiber, and dedicated broadband niches. Investors should therefore treat the public MNO statistics as highly reliable for the mass market, but incomplete for the broader connectivity economy.

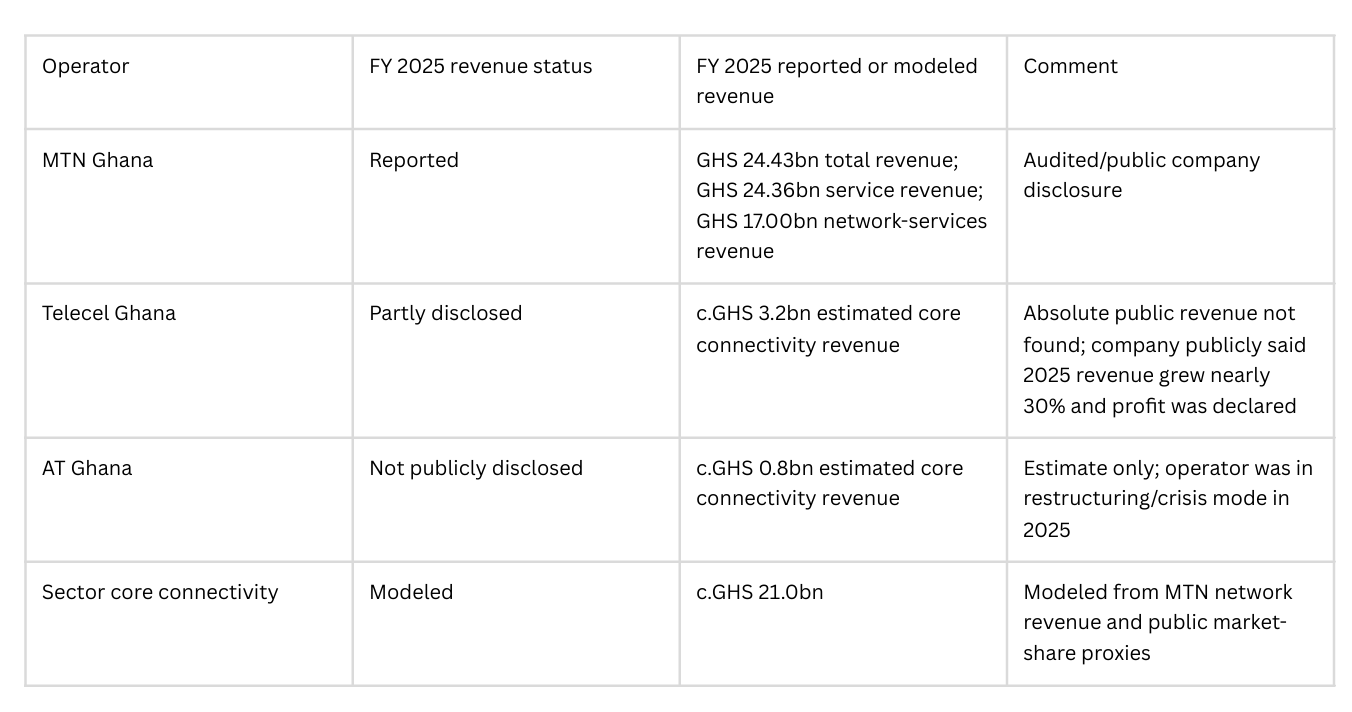

The most important disclosure constraint in Ghana is that MTN Ghana is public and publishes detailed financials, while Telecel and AT do not publish comparable granular revenue statements in the public domain used here. Accordingly, this report separates reported revenue from modeled revenue estimates. Reported revenue is used whenever possible; modeled revenue is used only where the user explicitly asked for company-level market size and where no primary public revenue disclosure exists.

MTN Ghana reported FY 2025 total revenue of GHS 24.43 billion, service revenue of GHS 24.36 billion, data revenue of GHS 13.36 billion, voice revenue of GHS 3.81 billion, EBITDA of GHS 14.69 billion, and total capex of GHS 6.41 billion. Telecel Ghana publicly disclosed that it recorded “nearly 30 per cent” revenue growth in 2025 and declared a profit, but it did not publish a comparable absolute revenue figure in the materials gathered here. AT Ghana’s public situation in 2025 was dominated by its tower-debt crisis and government-led transaction review, not by published financial disclosure.

For sector modeling, Africa Reporters Network estimates core connectivity revenue rather than total telecom-plus-fintech revenue. The proxy uses MTN’s reported FY 2025 network-services revenue of GHS 17.00 billion and scales it by estimated MTN share in connectivity revenue, using a data-heavy weight because MTN’s own revenue mix is now mostly data. Under that method, estimated FY 2025 Ghana core connectivity revenue is about GHS 21.0 billion, split approximately MTN GHS 17.0 billion reported, Telecel GHS 3.2 billion estimated, and AT GHS 0.8 billion estimated. This should be read as a modeled access-revenue view, not as an audited full-company revenue view.

Source note: MTN figures are reported; Telecel and AT numbers are estimates constructed from NCA market-share inputs and MTN segment weights, as described in the methodology paragraph above.

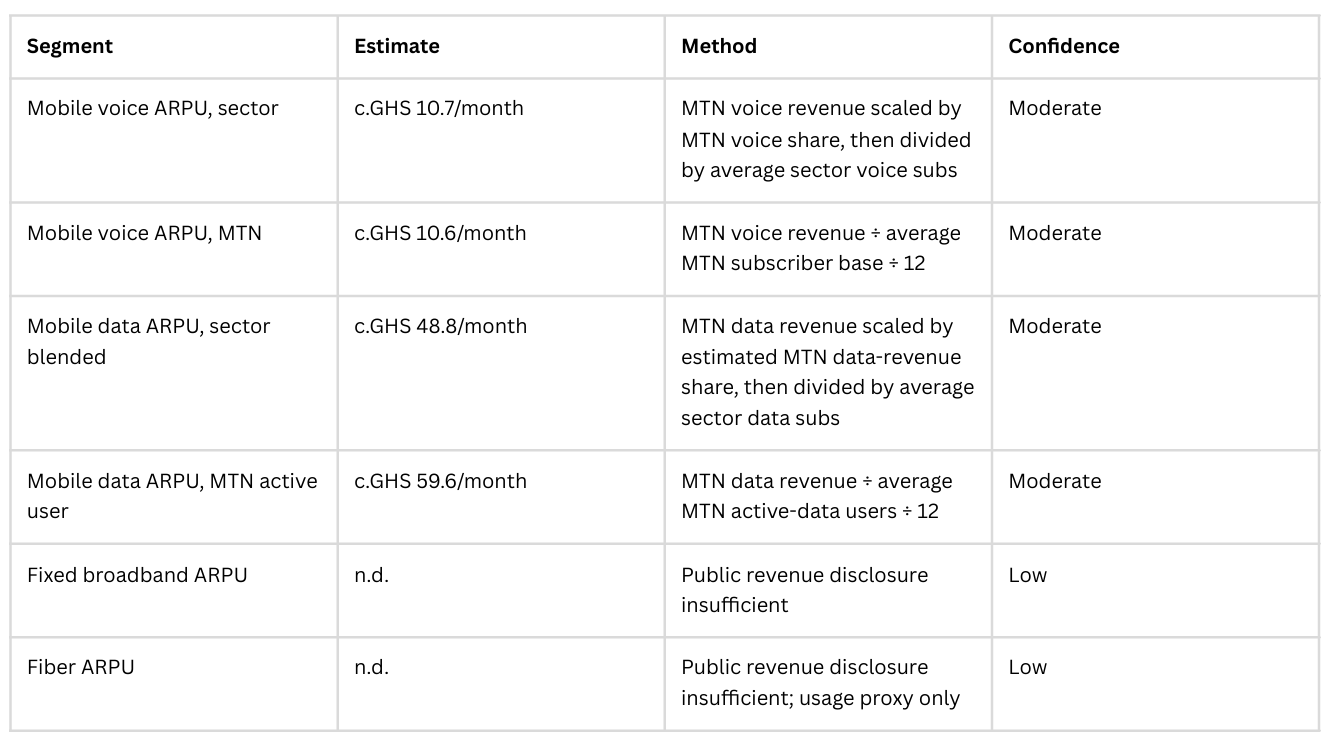

For mobile voice ARPU, I use a sector method anchored on MTN’s reported voice revenue and MTN’s public voice-share proxy. Estimated sector voice revenue is MTN voice revenue divided by MTN’s Q4 2025 mobile-voice share: GHS 3.806bn ÷ 72.92% ≈ GHS 5.22bn. Dividing by average sector mobile-voice subscriptions in 2025, approximated as the midpoint between Q4 2024 and Q4 2025 subscriptions, yields a sector mobile-voice ARPU of about GHS 10.7 per month per voice line. Using MTN’s own average subscriber base over the same approach yields an MTN voice ARPU of roughly GHS 10.6 per month.

For mobile data ARPU, the cleanest public revenue anchor is MTN’s FY 2025 data revenue of GHS 13.36bn. Because no regulator publishes data-revenue shares by operator, I proxy MTN’s data-revenue share with the midpoint between its Q4 2025 data-subscription share (79.68%) and data-traffic share (86.69%), or about 83.19%. That implies estimated sector mobile-data revenue of roughly GHS 16.1bn. Dividing by the average 2025 mobile-data subscription base gives a blended sector mobile-data ARPU of about GHS 48.8 per month per mobile-data line. For MTN alone, if one uses MTN’s average active-data-subscriber base rather than total data lines, implied active-data ARPU is about GHS 59.6 per month. This difference matters: blended line ARPU is lower because Ghana’s market contains many low-usage and multi-SIM lines.

For fixed broadband and fiber ARPU, the public record is much weaker. The NCA publishes subscriptions and traffic, but not revenue by operator or segment; MTN publishes total data revenue, but not a clean fixed/mobile split; and Telecel/AT do not publish comparable segment data in the source set used here. I therefore do not give a high-confidence numeric sector ARPU for fixed broadband or fiber. Instead, I provide a usage proxy: Q4 2025 total fiber traffic of 130,209 TB divided by average fiber subscriptions over the quarter implies roughly 169 GB per fiber subscription per month, versus about 12.9 GB per mobile-data subscription per month using the NCA’s own mobile-data usage table. That large usage gap is one reason fixed broadband can economically support higher monthly spend even when subscriber bases are small.

Source note: “n.d.” here means not derivable robustly from the public primary-source set used in this report, not that the metric is unknowable inside operators.

The short version is that voice is still cash-generative, but data is where growth, capital needs, and competitive differentiation now sit. The NCA’s Q4 2025 bulletin shows default voice tariffs unchanged at GHS 0.14 per minute both on-net and off-net, while MTN’s FY 2025 results show voice revenue up only 7.8%. MTN also said total minutes of use declined 2.9% year on year because of continued migration toward VoIP and digital communications. That is classic late-stage voice economics: low incremental network cost, good cash margins, but limited growth and structural substitution pressure.

Data is a different business. Sector mobile-data traffic reached 1,101,301 TB in Q4 2025, up sharply year on year, while MTN’s data revenue grew 48.8% in FY 2025 and MTN’s active data users rose 13.7% to 19.9 million. But data monetization requires continual spending on spectrum, RAN modernization, transport, IP core, caching, data centers, backhaul/fiber, tower power, and international capacity. MTN’s own numbers show this clearly: total capex was GHS 6.41bn in 2025, ex-lease capex was GHS 4.59bn, and ex-lease capex intensity was 18.8% of revenue.

Fiber sits at the premium end of the data business case. Its upfront cost is much higher because the hard part is civil works, right-of-way, ducting, last-meter build, customer premise equipment, and ongoing fiber-repair exposure. The World Bank notes that extending fixed broadband into rural and low-density areas is often commercially unviable because the infrastructure cost is high while revenue is low, and the ITU’s Ghana GEMS pilot explicitly characterizes FTTH acceleration as primarily an urban and suburban play, with rural connectivity relying more on enhanced 4G and satellite. In Ghana’s own 2024 industry report, fiber cuts reached 1,658 incidents, a reminder that passive infrastructure risk is not theoretical.

So the practical investment hierarchy is clear. Voice offers declining but still useful cash flow. Mobile data offers the fastest retail growth, but with heavier spectrum and capacity needs. Fiber offers the strongest quality-of-service and enterprise economics where density exists, but only in selected geographies. That is why Ghana’s best telecom assets are increasingly integrated assets: spectrum plus towers plus metro fiber plus enterprise distribution, rather than any one layer in isolation.

Fiber broadband is growing, but from a low base. The NCA reported 261,938 fiber subscriptions in Q4 2025, up 18.44% year on year from 221,153. Using the same quarterly population denominator the NCA uses elsewhere in the bulletin — 33,750,036 — implied national fiber-broadband penetration is about 0.78% of population. Fixed data subscriptions overall reached 175,458, or 0.52% penetration. Fixed voice, by contrast, fell to 265,236 subscriptions and 0.79% penetration, confirming that Ghana’s fixed network future is broadband, not fixed telephony.

Public fiber penetration by region or official urban/rural fiber subscriber splits were not found in the primary sources used here. The best official proxy is broader internet-access geography: ITU’s African broadband report states that in Ghana, 57% of urban households had Internet access in 2024 versus 23% of rural households, and the ITU Ghana GEMS pilot says accelerated FTTH in Ghana is mostly viable in urban and suburban areas while rural connectivity continues to lean on 4G and satellite. The right interpretation is not that rural fiber is absent, but that public evidence supports an overwhelmingly urban-biased commercial rollout pattern.

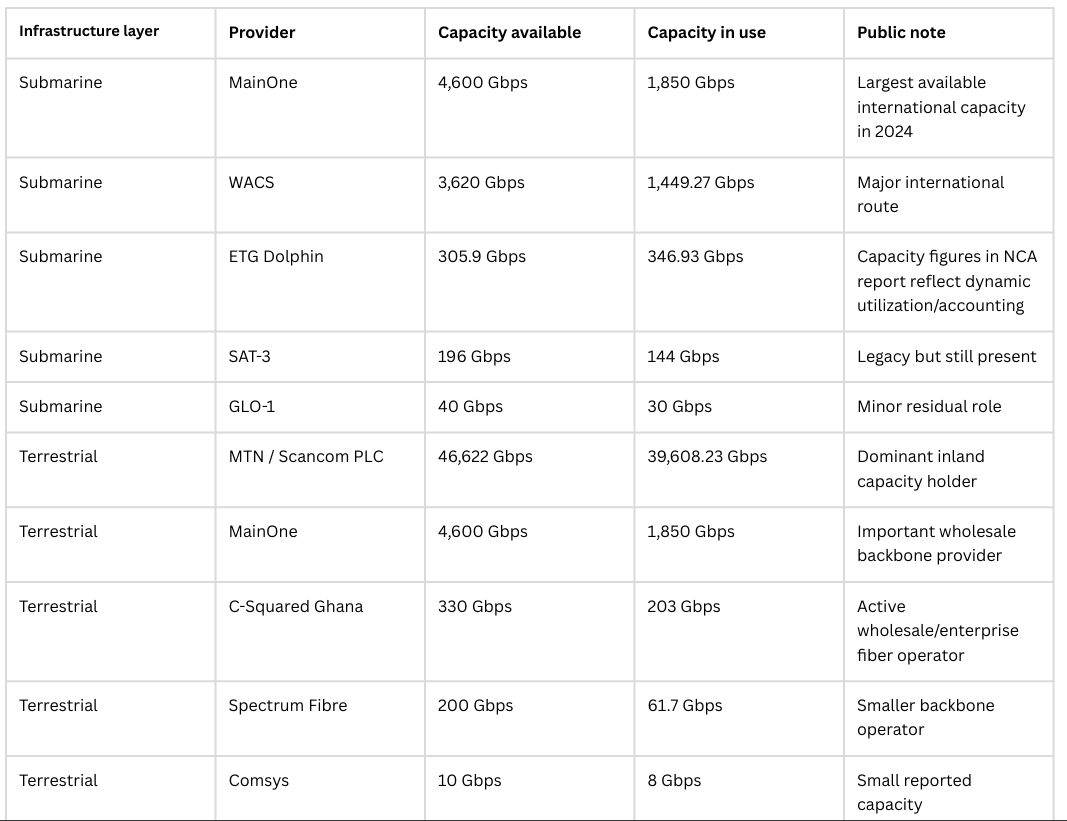

Ghana’s international and inland fiber base is much larger than its retail fiber-subscription base. In 2024, the NCA reported 8,525.9 Gbps of submarine capacity available and 3,646.2 Gbps in use. On the domestic side, the NCA reported 51,552 Gbps of terrestrial fiber capacity available and 41,661 Gbps in use, with MTN responsible for 90.44% of inland fiber capacity in use.

The retail FTTH/FTTB rollout status is most visible in MTN and Telecel’s subscriber growth. MTN’s fiber base rose from 139,267 in Q4 2024 to 171,862 in Q4 2025, while Telecel’s rose from 81,886 to 90,076 over the same period. This tells a specific story: Ghana’s fiber market is growing, but it is growing mainly through two integrated operators rather than through a broad open-access retail ecosystem. On the same evidence, AT has essentially no meaningful retail fiber position in current public statistics.

The major operational constraint is not only build cost but network fragility. The NCA counted 1,658 terrestrial fiber cuts in 2024, including 1,614 affecting MTN. It attributes these mainly to road construction, private development activity, illegal mining, cable theft, vandalism, and similar disruptions. In other words, the economics of Ghanaian fiber are shaped as much by civil-engineering and right-of-way risk as by telecom demand.

Ghana is one of the cleaner African cases of formal Starlink entry. The NCA approved SpaceX Starlink GH LTD in April 2024 after the Ministry approved a Satellite Licensing Framework, and the NCA said Starlink would officially start operations in Ghana by the end of August 2024. By Q4 2025, Starlink had reached 22,706 subscriptions. That base expanded from 7,696 in Q4 2024, implying roughly 195% year-on-year growth in its first full public year of operations.

The subscriber mix is heavily retail. In Q4 2025, Starlink’s Residential Lite plan had 9,666 subscriptions and the standard Residential plan had 11,536, together accounting for roughly 93.4% of the total. Priority and Enterprise plans were much smaller at 717 and 558 respectively. Geographically, Greater Accra alone accounted for 9,034 subscriptions, or about 39.8% of the national base, followed by Ashanti with 4,253, Western with 2,455, Central with 1,434, and Bono East with 1,419. That regional concentration suggests that Starlink in Ghana is not just a rural-access phenomenon; it is also an urban and peri-urban premium-connectivity product.

Current pricing strengthens that conclusion. The NCA’s 2024 Starlink FAQ said the standard Starlink kit cost GHS 5,390 in Ghana at launch, while current Starlink Ghana pages visible in June 2026 show Residential service starting from GHS 500 per month and a Mini Kit costing GHS 2,200. The same NCA FAQ also shows higher-end Priority pricing, including GHS 1,541 per month for 1 TB and GHS 3,082 per month for 2 TB. The practical takeaway is that Ghana has already seen meaningful entry-price compression in LEO broadband hardware, widening the addressable market.

The immediate threat profile is uneven. Starlink is not a major substitute for mobile voice. It is also not yet a direct substitute for low-income prepaid mobile-data users, who still buy connectivity in much smaller increments. But Starlink is already a credible substitute for four categories of demand: heavy-use households outside reliable fiber footprints; SMEs that need backup or branch connectivity; rural commercial users outside high-quality 4G coverage; and institutions that care more about uptime than about the cheapest nominal tariff. Ghana’s own geography supports that reading: retail subscriptions are concentrated in Accra and Ashanti, but meaningful adoption also appears in Western, Central, Eastern, Northern, and Bono East.

For local operators, the most exposed products are premium fixed-wireless offers, fragile SME links, and some parts of the fixed-broadband edge where fiber rollout is slow or civil works are unattractive. The least exposed products are mass prepaid mobile voice, low-ticket daily data, and bundled urban fiber where terrestrial operators can still deliver better unit economics and local service support. The strategic answer is therefore not to “beat Starlink on everything,” but to use terrestrial strengths — bundling, mobile-money integration, enterprise SLAs, on-ground service, and converged fixed-mobile offers — where LEO is weakest.

No high-confidence West Africa-wide Starlink subscriber total was found in the primary source set used here. The best hard subscriber count available here is Ghana’s NCA-published 22,706. Broader regional evidence only shows that Starlink was operational in 23 African countries by October 2025 and continued expanding afterward; that is useful context, but not a reliable West Africa subscriber count.

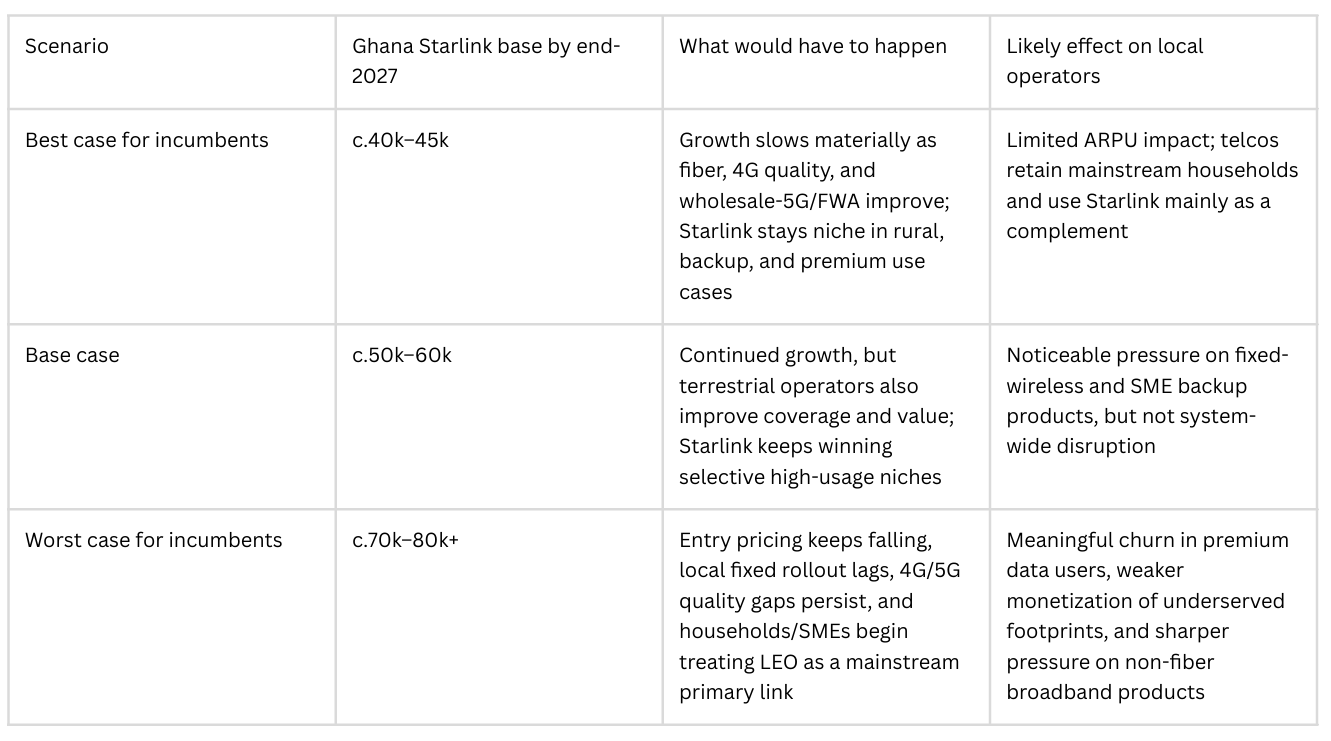

These are sensitivity cases, not forecasts. They are anchored on the published Q4 2025 base of 22,706 subscriptions and on the observed downward move in entry pricing from launch-era kit levels to current Residential/Mini pricing.

Ghana’s sector governance is active and increasingly interventionist. The NCA regulates the sector under Ghana’s electronic communications framework and publicly states that it seeks to promote fair competition, protect consumers, and ensure efficient use of telecommunications infrastructure. In 2020, it declared MTN a Significant Market Power operator. In March 2026, it opened a consultation on national-roaming wholesale rates explicitly linked to SMP remedies. In 2026 it also tightened mobile quality-of-service KPIs, and in March 2026 it moved to amend NGIC’s licence to remove the 5G exclusivity clause that had been part of the original wholesale-5G design. That is a real policy signal: Ghana is shifting from a tightly centralized wholesale 5G concept toward a more competition-oriented posture.

Spectrum and licence policy remain major capital-allocation variables. MTN Group disclosed that MTN Ghana paid the cedi equivalent of US$74 million in July 2025 for new spectrum assignments in the 1800 MHz and 2600 MHz bands, technology neutrality in 900/1800/2100 MHz, and licence-validity extensions to 2038. That is important for two reasons: it shows that spectrum remains expensive, and it shows that long-dated spectrum certainty is now being used as part of the investment bargain.

Recent M&A and restructuring activity has been intense. Vodafone completed its sale of Vodafone Ghana to Telecel in February 2023, with full retail rebranding completed by February 2024. AT, by contrast, has been the locus of instability: the Ministry’s own September 2025 briefing says government had bought AT in 2021 for US$1, that tower-power disconnections began in September 2025 over debt exceeding US$150 million, and that KPMG was appointed to advise on AT’s future and on government’s shareholding interests in Telecel. A June/July 2025 ministry briefing also said a major realignment was under way around a planned acquisition of a 60% stake in AT. As of the September 2025 ministerial statement, however, government stressed that the Telecel-AT arrangement then in place was not yet a merger or acquisition.

On investment, MTN is the cleanest benchmark. FY 2025 ex-lease capex intensity was 18.8% and headline EBITDA margin was 60.1%, placing MTN Ghana in a very strong position relative to the investment burden of the sector. Telecel, meanwhile, said in 2026 that it planned to increase network-infrastructure investment by about 150%, and it had already disclosed nearly 30% revenue growth and profit in 2025. That pairing — a dominant incumbent with high cash generation and a challenger entering a catch-up capex cycle — is typical of a market where competitive pressure exists, but mostly through investment asymmetry rather than price war alone.

The opportunity set for operators and investors is strongest in five areas. First, mobile data still has structural growth behind it because smartphone usage and traffic are still expanding. Second, fixed and metro fiber remain underpenetrated relative to urban demand. Third, enterprise and wholesale infrastructure have stronger pricing power than mass prepaid. Fourth, power optimization and passive-infrastructure management are critical because energy and site economics are as important as retail tariffs. Fifth, hybrid terrestrial-satellite products are becoming more attractive as customers seek resilience after years of dependence on terrestrial and submarine routes.

The main risks are equally clear. Market concentration can invite more intrusive ex ante remedies. AT’s unresolved future could create either a stronger challenger or a prolonged distressed overhang. 5G policy remains fluid after the move to strip NGIC’s exclusivity. Fiber cuts and civil works can destroy value in passive assets. Satellite competition will selectively pressure high-value broadband users if terrestrial rollout lags. And affordability remains a real constraint, especially outside dense urban zones where the economics of fixed build are weakest.

Some of the user’s requested metrics are not publicly observable with the same precision as MNO subscriptions. In particular, exact 2025 revenue for Telecel and AT was not publicly disclosed in the source set used here; fixed-broadband and fiber ARPU could not be derived robustly from public primary disclosures; non-MNO ISP market shares remain opaque in public regulator statistics; and I did not find a reliable primary-source total for Starlink subscribers across all of West Africa, only for Ghana itself. Older-brand exit dates — especially for the Celltel/Kasapa/Hutch/Expresso lineage — are also less consistently documented in the open record than the better-known Vodafone/Telecel and Airtel/Tigo/AT transitions.

.png)

Stay informed with the latest African media trends, job opportunities, and development news. Connecting Africa with global media and development partners.

.avif)

).png)

%20(1).avif)

.avif)